Atome is a regulated fintech platform offering Buy Now, Pay Later (BNPL) services in the Philippines. Its BNPL system allows Filipino consumers to split purchases into installments or delay payment for a short period without using a traditional credit card. The service is app-based, easy to access, and designed for users who want flexible payment options while maintaining visibility over their spending.

While Atome also offers a card-based product, this guide focuses specifically on Atome Buy Now Pay Later as a payment service, how it works, its costs, risks, and who it is best suited for. Understanding Atome BNPL as a financial tool helps users decide whether it fits their budget, lifestyle, and spending habits.

What Is Atome Buy Now Pay Later?

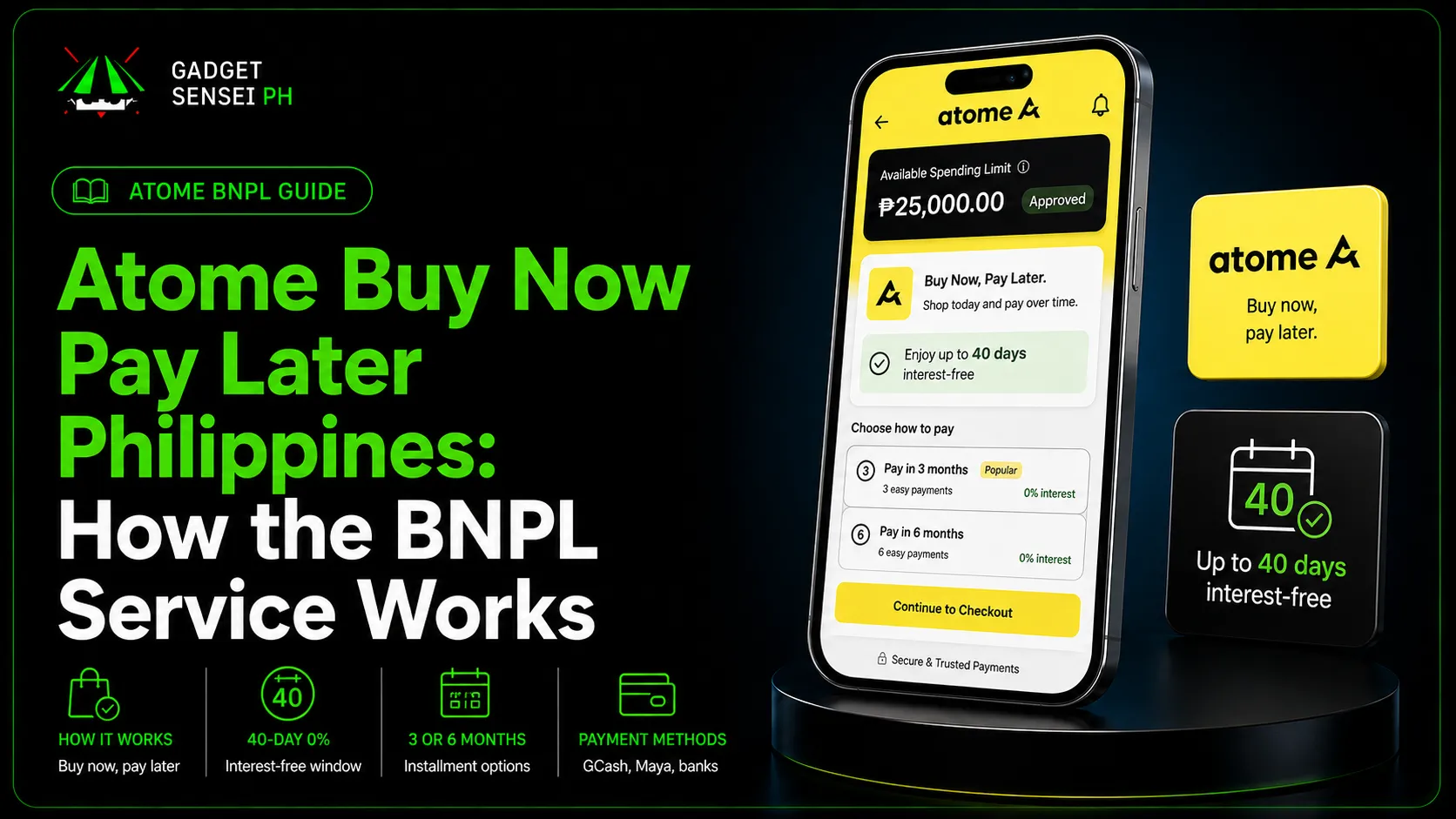

Atome Buy Now Pay Later is a short-term installment payment service that allows users to purchase items immediately and pay later, either in full within an interest-free window or through fixed installment plans. Instead of paying the full amount at checkout, the cost is recorded in the Atome app and settled on a later date.

The BNPL model is designed to make everyday purchases more manageable, especially for users who do not have access to credit cards or prefer not to use them. Atome evaluates users internally and assigns a spending limit, which refreshes as bills are paid.

It is important to note that BNPL is not free money. It is a form of short-term credit that requires disciplined repayment to avoid fees or account restrictions.

How Atome Buy Now Pay Later Works in the Philippines

Using Atome BNPL follows a straightforward process:

- Download the Atome Philippines App and register using a valid Philippine government ID.

- Complete account verification inside the app. Approval usually takes only a few minutes.

- Once approved, you are assigned a spending limit for BNPL purchases.

- Make a purchase using Atome at checkout or through supported payment flows.

- The purchase is added to your monthly statement in the app.

- Pay the balance in full within the interest-free period or convert it into installments.

Atome manages all transactions, billing, and repayment schedules inside the app. Users can see due dates, payment options, and total costs before confirming any installment plan.

For users who want BNPL access across more merchants and platforms, Atome also offers a separate card-based product, which is covered in detail in your Atome Card PH guide. This BNPL article focuses only on the service layer, not the card itself.

🎉 Win Up to ₱6,000 Cashback or an iPhone!

Sign up for an Atome Card using my link and get a chance to enjoy exclusive rewards. Registration is quick, easy, and 100% online.

👉 Register for Atome Card Now*Promos are subject to Atome Philippines’ terms and availability.

Interest-Free Period and Installment Options

One of Atome BNPL’s biggest appeals is its interest-free period, which is usually up to 40 days from the transaction date. If you pay your full balance within this window, no interest or financing charges apply.

For users who need more time, Atome allows conversion of eligible purchases into 3- or 6-month installment plans. When choosing installments:

- The app clearly displays the total payable amount

- Financing charges are shown before confirmation

- Monthly payments are fixed and predictable

This transparency helps users decide whether flexibility is worth the added cost. Paying in full remains the most cost-effective option, while installments offer budgeting convenience at a price.

Compared to cash, Atome BNPL allows you to delay payment without paying up front, which can help manage short-term cash flow. Unlike credit cards, Atome does not require a high income or credit history and does not charge annual fees.

However, credit cards may offer longer-term flexibility and credit-building benefits, while Atome BNPL is best suited for short-term installment purchases that can be repaid quickly.

Payment Methods Available to Filipino Users

Atome BNPL bills can be paid through several locally supported channels, making repayment accessible across the Philippines:

- InstaPay bank transfer from most Philippine banks

- E-wallet billers such as GCash and Maya

- Over-the-counter cash payments at partner outlets

- Linked debit or credit cards

- Atome Savings balance, if available

Among these options, InstaPay and Atome Savings are typically the most cost-efficient, as some payment methods may include processing or convenience fees. The Atome app provides step-by-step instructions for each payment channel.

Fees, Late Payments, and Financial Risks

Atome BNPL does not charge annual or membership fees. However, users should be aware of the following potential costs:

- Late payment fee of up to 5 percent of the outstanding balance

- Possible temporary account suspension if payments are missed

- Reduced spending limits for repeated late payments

- Financing charges on installment plans

- Foreign transaction fees for purchases made in other currencies

BNPL services are easy to use, but they can become expensive if bills are ignored. Users should treat Atome BNPL with the same discipline as a credit card or personal loan.

Comparing Atome BNPL vs Cash vs Credit Cards

Compared to cash payments, Atome BNPL allows users to delay payment and manage cash flow more effectively, especially for planned purchases.

Compared to credit cards, Atome BNPL:

- Has easier approval requirements

- Does not require income documents

- Has no annual fees

- Does not build credit history

Credit cards may be better for long-term financing, rewards, and credit-building, while Atome BNPL works best for short-term, controlled spending that can be repaid quickly.

Who Should Use Atome BNPL (and Who Should Avoid It)

Atome BNPL is suitable for Filipinos without credit cards, those who want installment options, and users who can reliably meet payment deadlines.

It may not be suitable for people who frequently miss bill payments, have unstable income, or struggle with impulse spending. BNPL should be treated as a financial tool, not extra income.

Common BNPL Mistakes to Avoid

Many BNPL users encounter problems due to avoidable mistakes, such as:

- Assuming all purchases are interest-free

- Forgetting payment due dates

- Using installments unnecessarily

- Ignoring small fees that accumulate over time

- Treating BNPL limits as extra money

To avoid these issues, users should set reminders, review payment terms carefully, and prioritize full payment whenever possible.

Frequently Asked Questions

What is Atome Buy Now, Pay Later in the Philippines?

Atome Buy Now, Pay Later is a BNPL service in the Philippines that lets users purchase items using the Atome Card and pay later either in full within the interest-free period or through installment plans.

How does Atome buy now pay later work?

Atome allows you to shop using the Atome Card, then pay your purchases later through the app. You can pay in full for 0% interest or split the amount into 3- or 6-month installments.

How do I use Atome buy-now-pay-later services for the first time?

To use Atome buy-now-pay-later services, download the Atome PH app, complete registration, activate your virtual or physical Atome Card, and use it like a regular Mastercard when shopping.

Is Atome Buy Now Pay Later available in the Philippines?

Yes, Atome Buy Now Pay Later is officially available in the Philippines and can be used at local and international merchants that accept Mastercard.

Does Atome Buy Now Pay Later charge interest?

Atome does not charge interest if you pay your balance in full within the interest-free period, usually up to 40 days. Interest applies only when you choose installment plans.

What is the Atome buy now pay later interest rate?

The Atome buy now pay later interest rate typically starts at around 2% per month for installment plans, depending on the selected payment duration and current offers shown in the app.

Can I use Atome Buy Now Pay Later for online shopping?

Yes, Atome Buy Now Pay Later can be used for online shopping by entering your Atome Card details at checkout on websites that accept Mastercard.

Can I use Atome Buy Now Pay Later in physical stores?

Yes, you can use Atome Buy Now Pay Later in physical stores by tapping or inserting your Atome Card at Mastercard-enabled terminals in the Philippines.

What payment methods can I use to pay my Atome bill in the Philippines?

Filipino users can pay their Atome bill using InstaPay bank transfers, GCash, Maya, over-the-counter payment centers, or linked debit and credit cards.

What happens if I miss an Atome payment?

Missing an Atome payment may result in late fees, reduced spending limits, or temporary account suspension, so it’s important to pay on or before the due date.

Is Atome Buy Now Pay Later safe to use?

Yes, Atome Buy Now Pay Later is generally safe to use when managed responsibly, as long as users understand the fees, interest, and repayment schedule.

Who should use Atome Buy Now Pay Later?

Atome Buy Now Pay Later is suitable for Filipinos who want flexible payment options, do not have a credit card, and can commit to paying installments on time.

Who should avoid using Atome BNPL?

Users who struggle with budgeting, frequently miss bill payments, or rely on borrowing for daily expenses may want to avoid BNPL services like Atome.